EU+UK Compound feed production in 2020 stable / Market Outlook 2021

Industrial compound feed production in the EU remained stable in 2020 despite the combined effect of the spread of animal diseases (ASF & AI) and the COVID-19 pandemic in 2020.

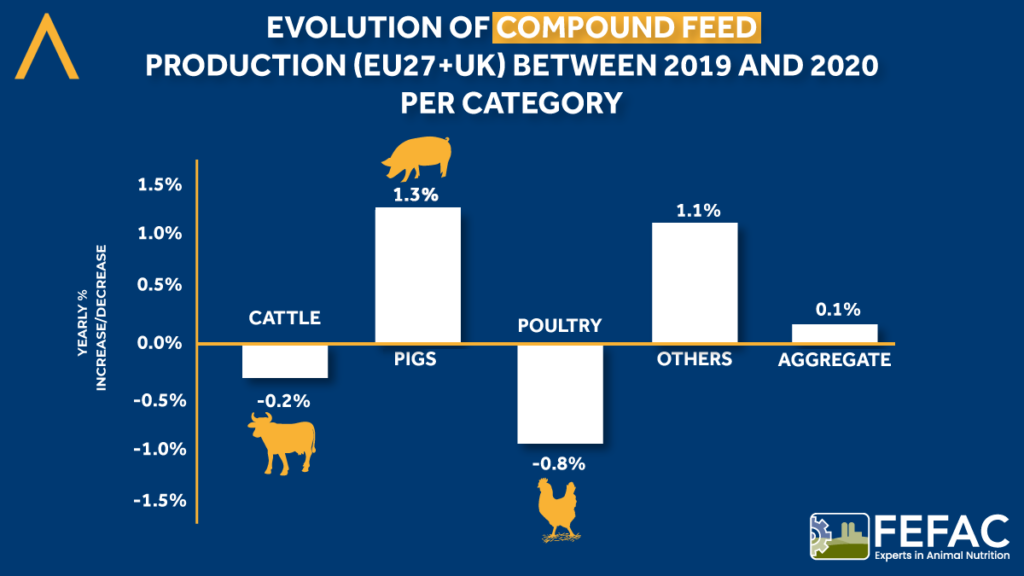

EU compound feed production (EU 27[1]+UK) for farmed animals[2] in 2020 is estimated at 164,9 Mio t., an incremental increase of 0.1% compared to 2019, according to data provided by FEFAC members.

Despite the COVID-19 pandemic and its heavy impact on several sectors including HORECA and Tourism, the European compound feed industry managed to keep its production at a stable pace, contrary to early predictions. While cattle & poultry feed saw a decline, all other sectors experienced production growth compared to 2019.

The decrease of 0.8 % in the poultry feed production, which is the first recorded in 10 years, is a result of the combined effect of the spread of Avian Influenza (HPAI) and COVID-19 lockdown measures. In 2020, there were two seasons of the HPAI epidemic in Europe[3] depressing the poultry sector. In earlier months of 2020, the disease was detected in PL, CZ, DE, SK, RO & HU while in autumn the disease hit the NL, DK, HR, FR, IR, SE, UK and again PL & DE. The most affected country was Hungary after the virus entered the area with a high density of ducks and geese holdings. COVID-19 lockdown measures and overall decrease in tourism had a negative effect especially in Spain where the poultry sector decreased its production substantially by almost 20% compared to 2019.

Cattle feed production slightly decreased by 0.2% mainly due to the indirect impact of COVID-19 and the closure of the HORECA chain (Hotel/Restaurant/Catering) that lead to a shift in consumer demand for products of animal origin. Still, the cattle feed tonnage did not fall as initially expected due to a drier than normal spring season and poor grass growth in several countries.

Despite the spread of African Swine Fever (ASF) in Europe and its impact on the pig sector, pig feed production increased by 1.3 % in 2020. This was mainly because several countries increased their exports to China benefiting from Germany´s export ban. Furthermore, due to the COVID-19 problems with slaughterhouses capacity, many farm animals stayed on the farms longer than necessary, which led to higher feed consumption. Compared to young animals, finishing animals have a higher feed conversion ratio (more feed is needed to produce one kg of meat/maintain the weight).

Looking at the market outlook for 2021, very low profitability characterised the pig and poultry sector the first months due to higher feed prices, linked to the global grain market rally starting in Q4 of 2020. An increasing number of Member States faces problems for EU exports of animal products due to the evolving AI & ASF situation. Overall, it is expected that market problems for animal products resulting from the combination of COVID-19, AI and ASF impacts will continue and as such impact the industrial compound feed production. Next to that, the impact of the EU Green Deal policy agenda and national authorities initiatives to tackle the environmental emissions (BE, NL – ammonia emissions) & welfare issues (DE) continue to create additional pressure on the EU livestock and feed sector.

[1] Without Luxemburg, Greece and Malta

[2] From 2016 on, FEFAC no longer includes dry petfood production in its statistics, considering that a large part of the production was missing in national statistics.

[3] https://ec.europa.eu/food/system/files/2021-01/ad_control-measures_hapai_chrono_2020_map.pdf